nj bait tax example

Section 1835-41 - Computation of credit for taxes paid to other jurisdictions a The following provisions shall govern the computation of the tax credit by reason of any income or wage tax paid to another state or political subdivision of such state under the New Jersey Gross Income Tax Act Act. Assuming there are two owners that each own 50 of the business each owner will get a credit of 5675 on its respective tax return.

Why New Jersey Should Require More Accounting Credits To Sit For The Cpa Exam

912 for distributive proceeds between 1000000 and 5000000.

. The BAIT program is intended to give New Jersey individual income taxpayers a work-around of the 10000 annual limitation on the. The PTEs distributive income is subject to tax at the following graduated rates for purposes of computing the BAIT. S corporation S has net income of 1000000 in 2020 and one individual shareholder A.

This law was passed in response to the Federal Tax Cut Jobs Act passed in December 2017 that restricted. Lets say that you own a business that has 3 members with shares of distributive income sourced in New. The elective entity tax is.

The New Jersey Business Alternative Income Tax also referred to as BAIT or NJ BAIT helps business owners mitigate the negative impact of the federal state and. This act creates an election for pass-through entities PTEs to pay New Jersey income tax at the entity level and creates a corresponding individual income tax credit for the members of the PTEs. We will now walk through an example to help understand the calculation of tax due.

That appears to be the moto of the NJ Legislature after passing the Pass-Through Business Alternative Income Tax Act the Act signed into law by Governor Murphy on January 13 2020. It modifies how the optional tax is calculated so that more income is subject to the tax thereby. New Jersey joined the SALT workaround bandwagon this year by establishing its Business Alternative Income Tax BAIT.

5675 for distributive proceeds below 250000. Signed into law in January the BAIT is a new elective business tax regime in which New Jersey PTEs partnerships limited liability companies and S corporations can elect to pay an entity-level tax. January 18 2022 Update.

3246 into law referred to as the Pass-Through Business Alternative Income Tax Act or BAIT Act. Using the table above tax is calculated on the 900000 as follows. The bill includes the following changes which are effective Jan.

How to File Like many other New Jersey taxes BAIT forms and payments must be submitted. New Jersey has enacted the Pass-Through Business Alternative Tax Act BAIT. Pass-Through Business Alternative Income Tax Act.

3246 or bill establishing the business alternative income tax BAIT an elective New Jersey business tax regime for pass-through entities PTEs. This extension includes the 2021 PTE Election 2021 PTE-100 Tax Returns 2021 PTE-200-T 2021 Revocation forms and 2022 Estimated Payments. Mechanics of the BAIT Election.

Each member can use the BAIT credit to offset their member-level tax liabilities. 1 Effective immediately the legislation allows New Jersey pass-through entities PTEs to pay tax at the entity level and permits owners of. To rectify the implementation issues with New Jerseys Business Alternative Income Tax BAIT a clean-up bill was drafted which has been signed by Governor Murphy.

On January 13 2019 the New Jersey governor signed S. Consider the following simplified example. For example if a pass-through business has New Jersey source income of 200000 the BAIT is 11350.

109 for distributive proceeds over 5000000. PL2019 c320 enacted the Pass-Through Business Alternative Income Tax Act effective for tax years beginning on or after January 1 2020. In response to federal tax reform enacted in December 2017 New Jersey was.

How to i elect to utilize the NJ BAITbusiness Alterative income tax program on an S corp tax return. Also if electing to calculate NJ BAIT the S corporation must apply gross income tax ie New Jerseys personal income tax methodologies for sourcing income while at the same time for purposes of reporting the net pro rata share of S corporation income to owners the S corporation will need to use corporation business tax methodologies. This new law allows pass-through businesses to pay income taxes at the entity level instead of the personal level.

The FAQs state that although an entity electing to be taxed under the BAIT must pay quarterly estimated tax it must also withhold taxes and pay estimates for its nonresident partnersshareholders to the extent otherwise. Each New Jersey resident members share of the entity level tax equals 565675050 2828375. For example if a pass-through entity with tax-exempt owners elects to pay the New Jersey BAIT then those tax-exempt owners should be able to claim a refund for the amount of tax paid by the pass-through entity13 Currently there is a not a prescribed refund form.

54A4-1 provides for a credit against the New Jersey gross. NJ PTE and BAIT returns due between March 15 2022 and June 15 2022 have an extended deadline of June 15 2022. This is the states second attempt to circumvent the 10000 federal cap on state and local tax SALT deductions imposed by the Tax Cuts and Jobs Act TCJA.

652 for distributive proceeds between 250000 and 1000000. The PTE only pays tax on state-connected income meaning New Jersey residents who are required to pay GIT on their everywhere ie un-apportioned income may obtain a credit from a PTE that has income from both within and outside of New Jersey that may be significantly less than their total state income tax liability. The new law creates an election for pass-through entities PTEs to pay at the entity level and creates a corresponding tax credit for its members.

As mentioned above the NJ BAIT calculation will be made based on the sum of all the member shares of distributive proceeds. On January 13 2020 Governor Phil Murphy signed into law Senate Bill 3246 S. The New Jersey pass-through entity tax took effect Jan.

By passing through a net amount of income reduced by the SALT deduction the owner is able to fully deduct their New Jersey taxes for federal purposes. Tax is imposed on the sum of each members share of distributive proceeds which is 900000. For New Jersey purposes income and losses of a pass-through entity are passed through to its.

For example if a PTE earns 20 of its income. Using the graduated tax schedule tax on 900000 would be 5656750. Phil Murphy signed legislation creating the Business Alternative Income Tax BAIT an elective entity-level tax on pass-through businesses for tax years beginning on or after Jan.

New Jerseys most recent guidance addresses some issues regarding estimated tax payments and calculating the BAIT. 13 2020 New Jersey Gov. 1418750 42380 900000-250000 650000 x 652 42380 5656750.

A BAIT Tax Example Calculation. Pass-Through Business Alternative Income Tax Act.

What Is Capital Gains Tax And When Are You Exempt Thestreet

Weekend Getaways To Ocnj Ocean City New Jersey Ocean City New Jersey

State Of New Jersey Combined Corporate Reporting Requirement Marcum Llp Accountants And Advisors

New Jersey Businesses Should Consider Salt Deduction Limitation Withum

Capital Gains Tax Under The American Families Plan Marcum Llp Accountants And Advisors

What Is Capital Gains Tax And When Are You Exempt Thestreet

New Jersey Businesses Should Consider Salt Deduction Limitation Withum

Reverse Sales Tax Audits

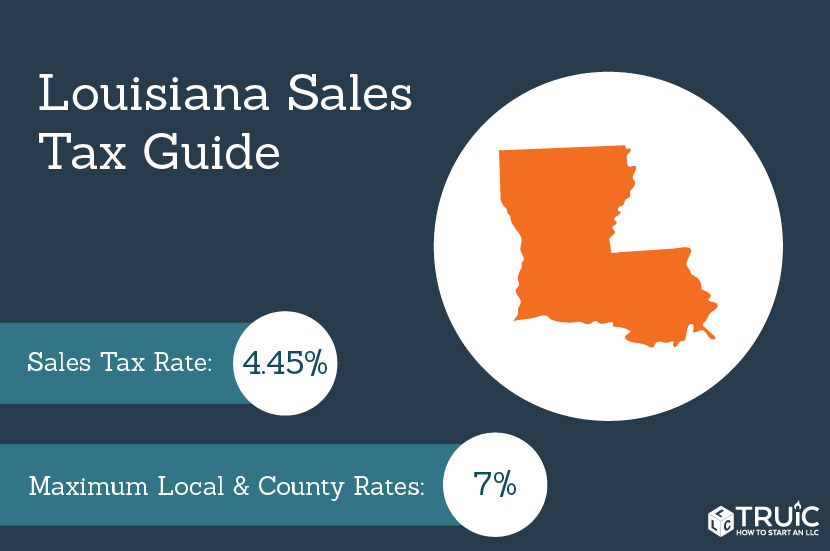

Louisiana Sales Tax Small Business Guide Truic

New Jersey Businesses Should Consider Salt Deduction Limitation Withum

Ny State Pass Through Entity Tax Can Save You Up To 40 8 Perelson Weiner

Catherine Mccabe Njdepmccabe Twitter

Recent Changes To The Interest Expense Limitation Rules

New Jersey Businesses Should Consider Salt Deduction Limitation Withum

Catherine Mccabe Njdepmccabe Twitter

Self Employment Tax Considerations For Llc Members Marcum Llp Accountants And Advisors

Nj Pass Through Business Alternative Income Tax Professional Services

Time To Check Your Withholdings Irs Updates Form W 4 Marcum Llp Accountants And Advisors

Reverse Sales Tax Audits